The word “uncertainty” tends to dominate economic news these days. Political uncertainty regarding the “fiscal cliff”, Washington’s self-imposed deadline that results in automatic tax increases and the repeal of the Bush tax cuts, turmoil in Europe, and a general slowdown in demand across Asia and the Eurozone have kept U.S. corporations on the sidelines in regards to hiring and new investment. An unclear picture on taxes, healthcare and a general lack of faith in Congress to get anything done has lead to companies hoarding cash despite posting record corporate earnings over the last few years. According to Thompson Reuters, the companies that make up the S&P 1500 index had over $1 trillion in cash or cash equivalents on their books at the end of Q2 2012. To put that in perspective U.S. GDP was $15 trillion last year.

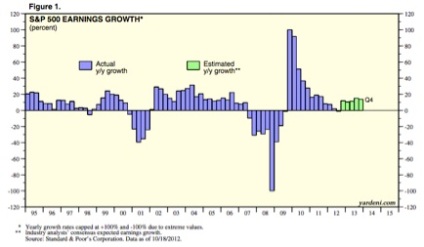

In addition to all the news about the fiscal cliff and chaos in Europe, earnings per share growth (or lack thereof) is another data point we should be paying attention to. As of September 30, S&P 500 estimates that Q3 2012 EPS growth will be -3.1% [UPDATE: As more companies have reported earnings this quarter, EPS growth has been revised to -0.1%.] This is significant because a negative turn in EPS growth typically indicates a recession. Of the last four times EPS went negative, three (1989, 2001, and 2007) pointed toward massive economic slowdowns and one in 1998 was a single quarter blip.

- EPS growth expected to go negative in Q3 2012, but analysts expect a bounce back in Q4 and 2013.

So is Q3 an outlier or the start of a slowdown? While analysts don’t believe we’ll see back-to-back negative EPS, they’ve begun revising their estimates downward. Since the end of the third quarter (September 30), analysts have reduced earnings growth expectations for Q4 2012 (to 5.6% from 9.3%), Q1 2013 (to 3.4% from 5.3%), and Q2 2013 (to 8.0% from 9.3%). A few trends might point to a more negative outlook.

From 2008 to 2011 corporate profits soared $578B, growing from a low point of $1.2T in 2008 to $1.8T in 2011. This was widely regarded as a jobless recovery as companies cut jobs and compensation, experienced low unit labor costs and significantly increased productivity per worker. Corporations also experienced relatively low commodity and material costs over this time period as shown in the graphs below:

But as you can see those trends have changed and corporations are experiencing increased material and labor costs, which provides one explanation a decrease in EPS. It makes sense that corporate earnings growth would slow during a recovery as companies spend excess cash (hiring new people, investing in R&D, etc.) to meet increased demand. But where will the demand come from this time around?

The consensus is that U.S. GDP growth will be relatively flat over the next few years, hovering around 2% to 3% growth for 2013 and 2014. For the rest of the world, the Eurozone is in turmoil and growth in China has slowed significantly. From 2008 to 2011, China’s GDP was growing at a double-digit rate, creating the demand necessary to offset recessions in the U.S. and Europe:

But with the U.S. economy stuck in a rut and demand in China and Europe waning, who will create the demand necessary to continue to fuel record earnings? If you look a little further back to earnings data from 2006, it paints a clearer picture of how important foreign demand has been to the earnings increase:

“Looking from 2006 – 2011 corporate profits grew by about $219 Billion. However, most of this growth came from outside of the U.S., around $182 Billion. U.S. domestic industries grew by only $36.6 Billion … While the U.S. growth figure is positive, the figure of $36.6 Billion includes a positive contribution of 42.1 Billion from “Federal Reserve banks”. This was over 17.5% annualized growth. All other domestic U.S. industries when aggregated together had a slight negative growth in profits from 2006 to 2011.”

This means over the time period from 2006 to 2011, corporate earnings derived from the U.S. were actually negative if not for the federal stimulus! It looks more apparent that the U.S. cannot drive corporate profits alone.

There is evidence that the slowdown around the world has started to hurt topline revenue for S&P 500 companies. While 70% of companies reported EPS above the mean estimate in Q3, 60% are reporting a revenue miss. Guidance doesn’t look good either. For Q4 2012, 72% of companies in the S&P 500 are reporting negative guidance, well above the long-term average of 61%. According to a survey by CEB, a membership based advisory firm, a little over half of managers expect production levels to increase in the next 12 months, down from 63% a year ago. Only 34% expect to hire in the coming year.

With all of the current risks in the market, you would think that the market would be cheap. There should be a correlation between negative guidance and stock prices (as there was until 2010), but the actual results have been the exact opposite:

It should be pointed out that sectors that are heavily tied to commodity prices (energy, materials, utilities, and industrials) make up the laggards of the group and commodity prices could be the culprit. There also might be some short-term fallout from insurance companies due to Hurricane Sandy, but this could be offset by increased production and investment in the rebuilding effort.

So is this past quarter a blip in the radar or the bearer of bad news? Is there a fundamental issue with the U.S. economy or a few sectors hurting earnings? Will there be a harsh correction in the market?

Uncertainty is most certainly driving corporate decisions and we’ve reached what Clayton Christiansen calls “The Capitalist Dilemma”. Christiansen explains this dilemma as the notion that executives and investors will fund three types of innovations: empowering, sustaining, and efficiency. Empowering innovations “transform complicated and costly products available to few, into cheaper products available to many”. By empowering innovations, companies spend money by creating jobs, increasing capacity to meet demand for new products (i.e. Model T, personal computers, etc). Sustaining innovations that simply replace old models with new ones (new HDTV to replace your old TV). This has a neutral effect on the economy because you’re eliminating your old product with a new one. Lastly, the efficiency innovations “reduce the cost of making and distributing existing goods and services”. Replacing 100 workers with machines in an auto plant would fall into the efficiency innovation category.

According to Christiansen:

“Ideally, the three innovations operate in a recurring circle. Empowering innovations are essential for growth because they create new consumption. As long as empowering innovations create more jobs than efficiency innovations eliminate, and as long as the capital that efficiency innovations liberate is invested back into empowering innovations, we keep recessions at bay. The dials on these three innovations are sensitive. But when they are set correctly, the economy is a magnificent machine.”

In the current state of the U.S. economy the balance is off. Investments in efficiency have liberated capital, but have only lead to investments in more efficiency thus decreasing the number of jobs. Executives running Fortune 500 companies have been taught to do (and are doing) what’s right for their own companies and shareholders. Investing in efficiency innovations are what lead to record corporate profits and sky-high stock prices over the last few years. And there in lies the paradox. Uncertainty in the market has disrupted the balance between empowering innovation and investing in efficiency. We currently have a glut of cash and a lack of qualified workers, yet companies are refusing to spend money on training new employees (companies also blame the education system and want reform, i.e. the Government to pay for it, but that’s a whole different blog post). Until the fiscal cliff is resolved and there’s stability in Europe, companies are going to continue to do what’s right for them and that means keeping balance sheets flush with cash. Until companies have the incentives to invest in innovation, the U.S. economy will continue to be stagnate and unemployment will remain high.

Cutting costs and investing in efficiency can only go so far. Without an uptick in demand from the U.S. and slowing growth abroad, we may see earnings take a hit in the near future. All of this coupled with Congress’ “stellar” track record on determining economic policy, I would tend be a bit more pessimistic in 2013.

{kind=link}